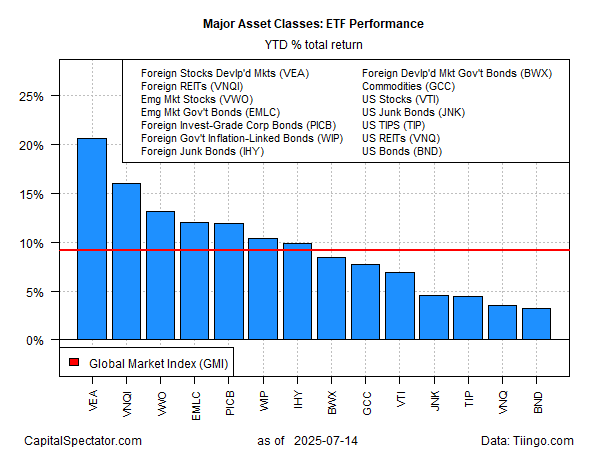

Judging by the headlines, there’s rather a lot to fret about. But when markets are anxious it’s not apparent within the year-to-date outcomes for the main asset courses, that are posting across-the-board positive aspects in 2025 through a set of ETFs via Monday’s shut (Jan. 14).

Main the bull run: shares in developed markets ex-US (VEA). This slice of worldwide equities tops the sphere with a 20.1% complete return thus far this 12 months. That’s properly forward of the second-best performer: international actual property ex-US (VNQI), which is up 16.1% 12 months to this point.

{kind=link}

US property are relative laggards: American shares (VTI) are forward by 6.9%. US junk bonds (JNK), actual property funding trusts (VNQ), and investment-grade US bonds (BND) are posting even softer positive aspects.

Though returns fluctuate broadly for 2025, it’s placing that there aren’t any losers. Optimism, in brief, is widespread.

One cause is that rates of interest stay regular. Regardless of worries about tariff-related inflation, the benchmark 10-year Treasury yield continues to commerce in a variety. This yield settled at 4.44% yesterday, a middling degree for the 12 months thus far.

A break above the latest excessive – roughly 4.60% for the 10-year — may change the calculus and persuade the group to rethink its comparatively upbeat assumptions in regards to the close to time period.

In the meantime, a latest survey of seven,000 traders by Natixis Funding Administration finds that expectations for long-term returns are sky excessive. As Morningstar reviews: US traders responding to the survey stated they anticipate shares to generate long-term returns of 12.6% per 12 months above inflation.

That appears far too rosy to this observer. As I wrote just a few weeks in the past, a mannequin I run for TMC Analysis, a unit of The Milwaukee Firm, estimates US fairness efficiency will likely be within the low-5% vary for the last decade forward, or roughly half of the ten%-12% vary for annualized ten-year efficiency for US shares since 2024, primarily based on the on the common of 5 fashions.

Evidently traders within the Natixis survey are utilizing latest historical past as a information to handle expectations. That’s normally a mistake. However maybe this time is completely different. Possibly, however put me down as skeptical.

Keep forward of the curve with NextBusiness 24. Discover extra tales, subscribe to our e-newsletter, and be part of our rising neighborhood at nextbusiness24.com