New research reveals how U.S. sanctions, tariffs, and policy uncertainty are influencing central bank reserve choices — shifting weight from the dollar toward gold and alternative currencies.

The dominance of the U.S. dollar as the world’s primary reserve currency is facing fresh scrutiny. Rising geopolitical tensions, economic sanctions, and policy uncertainty have prompted many central banks to reconsider their currency holdings, with gold increasingly emerging as a preferred store of value. Recent studies suggest that financial sanctions and tariff disputes have already dented the dollar’s share in global reserves. Although the dollar remains strong, shifts in strategy could signal the early stages of a multipolar reserve future.

Is gold supplanting the greenback? Did the usage of sanction by the US cut back holdings of {dollars} by focused central banks? Did the 2018-19 tariffs cut back holdings of {dollars} by international locations hit with Part 232 tariffs? Jeff Frankel, Hiro Ito and I tackle these questions in a new paper.

We analyze the determinants of particular person central financial institution holdings of worldwide reserves, as shares of gold, greenback, euro, pound, yen and yuan, over the 1999-2022 interval. We increase normal financial determinants of dimension, change charge volatility, foreign money pegs and bilateral commerce with bilateral political/financial variables reminiscent of disagreement in UN voting, army alliances, and monetary and commerce sanctions. These variables increase uncertainty measures reminiscent of international Financial Coverage Uncertainty, US financial and commerce coverage uncertainty, and the VIX. As well as, we examine whether or not the US imposition of tariffs in 2018 had any measurable affect on greenback and different holdings. We conclude that monetary sanctions and commerce coverage uncertainty have a statistically and economically vital impact on holdings of the US greenback. US tariffs had an economically – however not statistically – vital affect on shares of international change reserves: greenback shares fell by 2.1% and different shares rose by 0.8%. These findings can inform the controversy relating to a number of the advantages and prices of utilizing such geo-economic insurance policies.

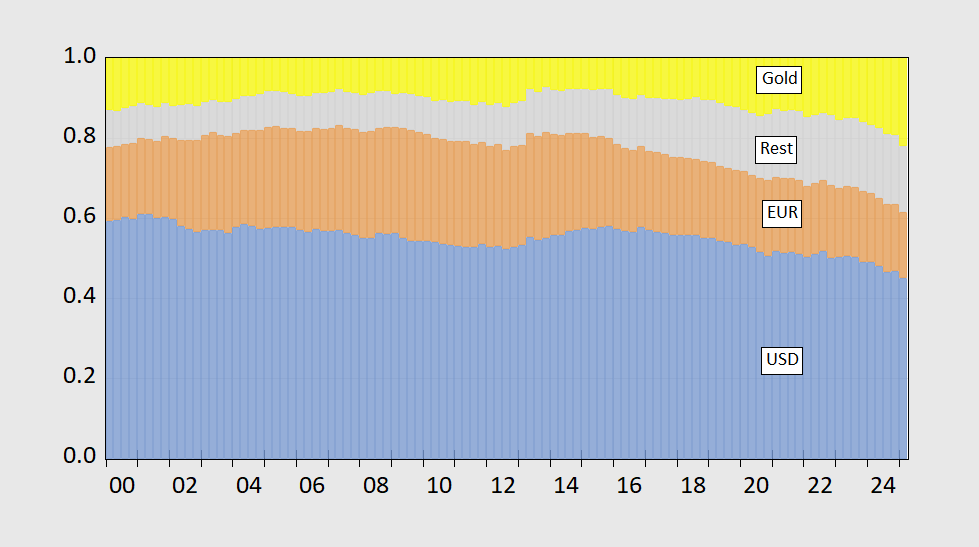

To research these questions, we rely in particular person central financial institution information, as utilized in Chinn, Frankel and Ito (JIMF, 2024). On this manner, we are able to distinguish between what’s occurring on the mixture stage (determine 1 beneath) and on the particular person financial institution stage (illustrated by median holdings, determine 2).

{kind=link}

Determine 1: USD shares of fx and gold reserves (blue bars), EUR (tan), all different (grey), and gold (yellow). USD(EUR) share assumes 60%(35%) of unallocated reserves are in USD(EUR). Assumes amount of gold holdings keep fixed in 2025Q, and noticed . Supply: IMF COFER, World Gold Council, and creator’s calculations.

Determine 2: Median shares of every foreign money or gold as a share of whole reserves, utilizing Ito-McCauley dataset. Supply: Determine 3, Chinn, Frankel and Ito (2025).

USD and EUR shares match up okay, however gold is a higher share in common than in median.

Whereas we don’t verify a job for the Part 232 tariffs (on aluminum and metal in 2018-19 in lowering greenback holdings, it’s vital to recall that these tariff revenues barely registered as a blip, in comparison with the present efficient tariff charges of close to 10%.

Moreover, the commerce coverage uncertainty that attended the Part 232 and Part 301 tariffs had a measurable affect on central financial institution holdings.

Keep forward of the curve with NextBusiness 24. Discover extra tales, subscribe to our e-newsletter, and be a part of our rising neighborhood at nextbusiness24.com