Disclaimer: Except in any other case acknowledged, any opinions expressed under belong solely to the writer.

The price of resale HDB flats stays one of many hottest subjects in Singapore and a supply of hysteria for a lot of Singaporeans. A rising variety of flats are promoting for over S$1 million, although the primary such transaction was recorded already again in 2012.

For a lot of the previous 13 years, these gross sales have been extra of an exception than the norm. Nonetheless, that has begun shifting along with the acceleration of worldwide inflation in 2022 and the spike in native demand for spacious housing following the experiences of the pandemic and the recognition of work-from-home preparations.

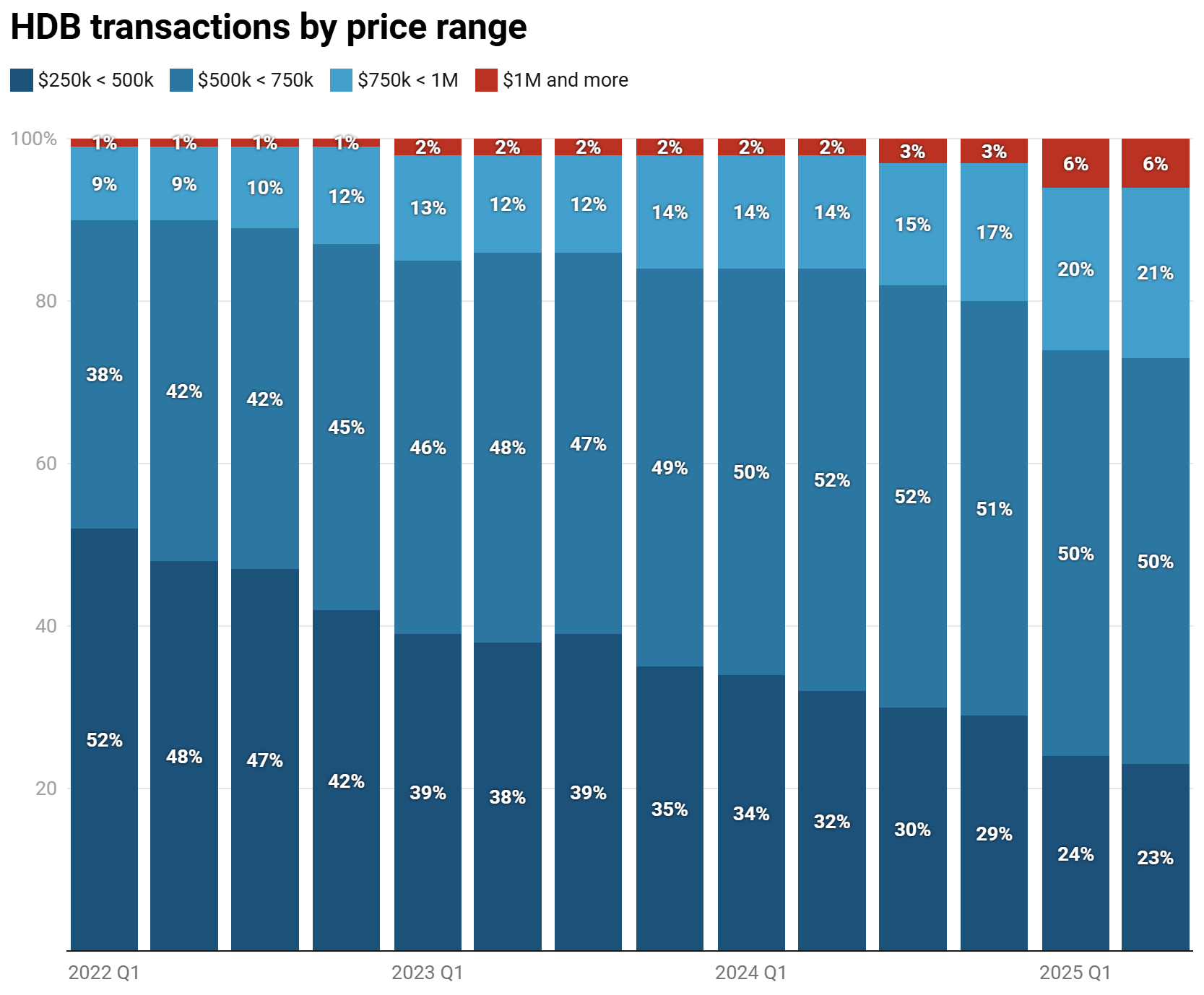

From below 1% as just lately as 2022, the share of million greenback transactions has steadily elevated, multiplying to over 6% in early 2025, already doubling in comparison with 2024.

{kind=link}

2024 noticed 1035 million greenback HDB houses bought, whereas 760 such transactions have already been recorded in simply the primary six months of 2025.

What’s extra, extra 21% fall throughout the vary of over S$750,000 to S$1 million, that means that, on the present tempo, they too may quickly cross into the million and over class. That’s over 1 / 4 of resale HDBs.

There’s actually no motive to worry, nonetheless, as a result of a gradual rise of housing costs isn’t solely largely useful however in some ways even mandatory for your complete system to work as supposed.

The pure state of the financial system

Identical to at present we’re watching costs creeping over six figures, 45 years in the past we noticed them strategy 5 figures for the most costly government flats provided by the federal government.

Whereas it’s not the resale market per se, these have been the worth tags earlier than the BTO period and again then, the costs between major and secondary markets didn’t differ an excessive amount of.

This desk is from mid-1979 and, on the time, the median family revenue of a Singaporean family was below S$990, in comparison with S$11,297 at present (practically 12 instances extra).

Over time the costs of comparable flats available on the market have additionally elevated by an element of 10 or extra. Erstwhile S$50,000 has change into S$500,000 and S$100,000 is now S$1 million and above.

That mentioned, residing requirements have enormously improved since then as effectively. Would you want to return to the Eighties, with outdated development requirements (together with barely any lifts), no MRT community connecting HDB cities, very restricted amenities and far, a lot decrease pay?

As incomes have gone up in tandem with housing, it’s their proportion to the worth of the flat that basically issues. That is why, with median transacted costs of below 5 instances the annual family revenue, Singapore’s HDB market is the second most reasonably priced wherever in your complete Asia-Pacific (and, actually, the world, since few main developed cities come even shut).

The median transacted value for a resale HDB in 2025 is round S$630,000.

It has to extend by one other 59% to cross S$1 million. But when family incomes do the identical, reaching round S$18,000 per 30 days, will it actually matter? Relative affordability of HDB housing goes to stay the identical.

It’s taken simply 13 years for them to rise by that a lot, from over S$7,000 in 2011 to over S$11,000 in 2024. So, we might be million greenback flats turning into the norm by mid to late 2030s.

Inflation eats the worth of cash—together with your money owed

Whereas we’re speaking in regards to the adverse influence that inflation has on the financial system and the worth of our incomes, it’s straightforward to overlook that it cuts each methods. And for those who occur to be in debt, you’re going to welcome the fast enhance in worth of the asset you bought with the borrowed cash.

That is significantly useful for housing, since few individuals pay the complete value in money and mortgages are the most affordable loans available on the market.

Inflation in condominium costs—particularly when, like now, client inflation is below management—enormously advantages debtors and helps them repay dues earlier or at the least makes their burden comparatively decrease with time.

Since overwhelming majority of Singaporeans already personal their houses, and about 80% stay in HDBs, they need to welcome the continued value rally. On the similar time, those that try to purchase and complain about how costly it has gotten, ought to really hope it will proceed, to allow them to profit from it in the long run as effectively.

Particularly as housing is a essential aspect of retirement planning.

The spine of your pension

As prices of life rise over time, the very last thing you need is the worth of your property to stay flat. On the floor, it would appear to be it shouldn’t matter. You reside in a single place and it doesn’t actually have an effect on you the way a lot it’s price.

Nonetheless, most retirees may be keen to downgrade from a big house to a smaller one as soon as their youngsters are out of the home, and use the distinction in value to complement their pension. And, opposite to common perception, lease decay doesn’t erode the worth of HDB houses as a lot as believed, with some houses with barely 50 years on their lease left promoting for seven figures in recent times.

Dropping from a 1000 sqft. condominium to 700 sqft. at roughly the identical per foot value, ought to internet them a 30% distinction. At S$1 million it’s S$300,000 however at S$600,000 it’s simply S$180,000.

Below low value situations, their new condominium can be significantly cheaper, however their internet achieve a lot smaller, leaving them with much less cash of their silver years.

In fact, if we may freeze the costs of all the pieces available in the market, it might not matter in any respect. However, as I mentioned, client items and providers get steadily dearer with time. Everyone knows this.

If flats don’t comply with—or, even higher, outpace—their costs, then Singaporean pensioners hoping to depend on their houses for an additional windfall after they cease working will likely be left tens or lots of of hundreds quick.

And since everyone goes to retire in the future, it’s best to hope that resale HDBs proceed to understand.

The proper steadiness

Paradoxically, it’s not within the public curiosity for flats to change into both very low cost or very costly. The candy spot is someplace round 4 to 5 instances of the annual family revenue.

Ideally, they need to comply with incomes (so that each new entrant faces the identical relative situations as his mother and father did) and develop at the least a bit quicker than client costs (in order that the cash, when you monetise your condominium partially or in full, should purchase you greater than earlier than).

If housing turned cheaper over time, it might eat into the wealth of pensioner households. Conversely, if it turned dearer, it might decrease the residing requirements and buying energy of youthful generations, who will likely be compelled to pay a higher share of their incomes on lodging.

In fact, quick time period fluctuations over a number of years are certain to occur, however so long as they’re smoothed out over the long run, this vital steadiness is maintained.

Which is why it’s not absolutely the value that’s vital.

It doesn’t matter if a flat prices S$1 million or S$2 million, or much more in some unspecified time in the future sooner or later—however how these costs evolve in relation to incomes and client costs. And that their relationship stays secure over time.

- Learn different articles we’ve written on Singapore’s present affairs right here.

Featured Picture Credit score: lteck/ depositphotos

Keep forward of the curve with NextBusiness 24. Discover extra tales, subscribe to our e-newsletter, and be a part of our rising group at nextbusiness24.com