Tales from the Employment State of affairs launch for July: (1) July Institution employment change beneath consensus; (2) Revisions make traits slower; (3) Provides knowledge indicating a slowdown.

{kind=link}

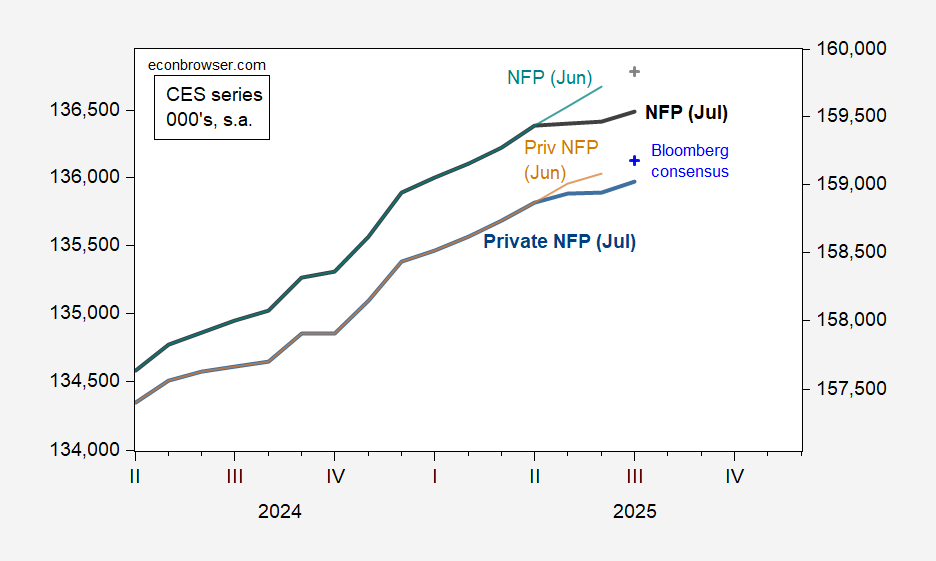

Determine 1: Nonfarm Payroll Employment, July launch (daring black, proper log scale), implied Bloomberg consensus (grey +, proper log scale), June launch (teal, proper log scale), Non-public NFP, July launch (blue, left hand log scale), implied Bloomberg consensus (blue +, left hand log scale), June launch (tan, left hand log scale), all in 000’s, s.a. Implied Bloomberg estimates calculated by iterating consensus change on prime of June launch figures. Supply: BLS, Bloomberg, and writer’s calculations.

Whereas one statement doesn’t make a pattern (+73K consensus vs. +106K for NFP), three observations may. We don’t make judgments on the premise of 1 preliminary statement as a result of the Imply Absolute Revision going from first to 3rd revision over the 2022-24 interval is about 40K. Therefore, it’s very doable that in two month’s time, the third launch for July’s knowledge might find yourself being above consensus. Nonetheless, given the revisions within the earlier months knowledge, it seems like a deceleration.

Right here’s an image of a number of collection depicting the slowdown alongside different dimensions of the labor market, and different financial indicators:

Determine 2: Month-to-month GDP (black), personal nonfarm payroll employment-ADP (blue), civilian employment w/smoothed inhabitants controls (mild blue), combination hours (mild inexperienced), consumption (tan), private revenue ex-transfers (pink), actual retail gross sales (purple), all in logs 2025M01=0. Actual retail gross sales is 3 month centered transferring common of retail gross sales, divided by chained CPI. Supply: S&P World, ADP-Stanford, BLS, BEA, Census, and writer’s calculations.

This appears to have been taken by the market as signaling a slowdown. The CME implied Fed funds fee dropped from 4.3% to 4.2% going from yesterday to right this moment at 10AM CT (though admittedly the Trump tariff bulletins may need had some influence as effectively). Betting markets are sending the identical message:

Supply: Kalshi, accessed 8/1/2025 10AM CT.

Assuming the higher than 25bps lower group is indicating 50bps, then the implied drop in September is 0.2 proportion factors.

Keep forward of the curve with NextBusiness 24. Discover extra tales, subscribe to our publication, and be a part of our rising group at nextbusiness24.com